Recent changes

- 2026-05-12

- Added §5.4 "What Counts as a Megawatt" — methodology section on the ELCC framework spread across utilities (Avista's 82% vs PSE's 16% on the same 4-hour battery; WRAP, NWPCC, and PacifiCorp framework variance). Includes Figure 5.4.

- Renumbered old §5.4 "The Coordination Gap" to §5.5.

Section 1: Two Futures

Section 1 lays out two futures for the Pacific Northwest grid. The first — the Collision Scenario — is what happens if the region’s institutional architecture continues unchanged. The second — the Coordination Scenario — is what becomes possible if the architecture shifts. Both are constructed from the same physical resources, the same demand growth, the same weather patterns. The fork is institutional, not technological.

1.1 The Collision Scenario: January 2032

Imagine January 10, 2032 in Seattle. A weakened polar vortex has allowed arctic air to spill south across British Columbia. A blocking ridge of high pressure over the Gulf of Alaska holds the cold in place, preventing the usual parade of mild Pacific storms from pushing it out. Dense, frigid air pours through the Fraser River valley into the greater Salish Sea.

Temperatures in Seattle drop to 16 degrees Fahrenheit. Cities across Western Washington have been below 20 degrees for five consecutive days. Families turn up the heat. Electric vehicles draw from the grid on the coldest mornings. Across the region, the system sets an unprecedented peak energy demand.

And then the same high-pressure ridge that trapped the arctic air does something else: it flattens the pressure gradients that drive wind. Turbines across the Columbia Basin slow, then stop. Low, heavy clouds settle over the region, blocking what little winter sun reaches this latitude in January. German grid operators have a word for this condition, the simultaneous collapse of wind and solar generation under a stagnant high-pressure system: Dunkelflaute, the dark doldrums. European grid planners have spent a decade learning to fear it. In the Pacific Northwest, which has built its decarbonization strategy around the same variable resources, the term barely registers. Researchers at Pacific Northwest National Laboratory studied four decades of hourly weather data across the continental United States and found that compound renewable energy droughts, periods when wind and solar fail together, occur in every region.

The PNW’s energy droughts tend to be shorter than California’s (hours rather than days), but they arrive during winter high-demand events when the grid has the least room to absorb them. And in the Pacific Northwest, the dark doldrums come with a third dimension that Germany does not face: when drought years have already drawn down the Columbia River system, hydropower cannot fully backstop the failure of wind and solar. The region faces a three-resource drought and across utility control rooms, the alarms sound as cross-state transmission lines reach the maximum energy they can carry and demand continues to climb.

In January 2024, the Pacific Northwest experienced exactly these conditions. Between January 10 and 17, temperatures in Seattle bottomed at 15 degrees, Portland hit 12, and Spokane plunged to negative 10. Regional power demand peaked at 35,594 MW, the highest load since the aluminum smelters left the system after the Western Energy Crisis of 2000-2001. Wind showed up on January 13 with roughly 1,000 MW of production, then tapered to near zero for the remainder of the week. The region survived by importing over 4,900 MW from California, the Desert Southwest, and the Rockies, while the Bonneville Power Administration (BPA) coordinated emergency operations with the Army Corps of Engineers and the Bureau of Reclamation to squeeze every available megawatt from the federal dams. Even then, BPA was managing the river to minimum flows due to a low water year, and the requirement to save water above Grand Coulee for spring fish operations limited how much additional generation the dams could provide. The backup system was itself running on fumes.

What has changed by 2032 is the system’s capacity to respond. Every utility in the region is drawing its full allocation of power from BPA. The Contract High Water Mark, the ceiling on cheap federal hydropower that each utility locked in back in 2025, is binding. If a utility needs to purchase energy above the ceiling, costs will, at minimum, double. BPA declares a system emergency on day two.

Every utility turns to the market. But the market is split. BPA operates in Markets+. Portland General Electric and PacifiCorp are in EDAM. Scheduling power across the seam between these two competing platforms adds hours to what should be real-time transactions. Prices on both sides spike past $500 per megawatt-hour, then $1,000. In January 2024, a single month of emergency market purchases cost Snohomish PUD ratepayers $45 million. This event will cost multiples of that, spread across every utility in the region.

Then the gas system fails. The same cold that created peak electric demand constrains the fuel supply to the region’s natural gas generators, the plants that were supposed to backstop the grid when hydro and the market fell short. This nearly happened on the day of peak demand during the 2024 event, when a fiber-optic network failure nearly caused an outage at Jackson Prairie, the region’s largest gas storage hub. Now imagine a more permanent failure.

Rolling blackouts begin on day three. Tens of thousands of customers across western Washington lose power in rotating outages as system operators struggle to balance a grid that has run out of options. Emergency operations at BPA face the same choice the agency confronted in 2001: ramp the dams to full generation and sacrifice future salmon survival, or maintain fish protections and extend the blackouts.

In 2001, when the region last faced this choice, the salmon lost. Juvenile steelhead survival rates on the Columbia dropped from 40 to 70 percent in normal years to roughly 6 percent. Treaty-protected fishing rights held by the Yakama, Nez Perce, Umatilla, and Warm Springs tribes were overridden by an emergency that the system’s own planning failures had created. Those rights are the foundation of tribal economies and predate the federal hydroelectric system by centuries. The Columbia River Inter-Tribal Fish Commission (CRITFC) predicted this would happen again. Speaking to the Northwest Power Council in April 2022, Ed Sheets put CRITFC’s concern plainly: “if the lights are about to go out, the salmon protections will go out before the lights.”

The costs to utilities, and by extension anyone paying an energy bill, do not end when the cold breaks. Emergency market purchases, emergency gas procurement, infrastructure damage, and deferred maintenance flow into the next rate case. Utilities that planned independently, each assuming market access that evaporated when everyone needed it at the same time, passed those costs to ratepayers. The desperate attempts individual utilities had made to adapt and expand the system, to meet the compound pressures of growing demand and worsening climate events, are set back further by backlash and burned budgets.

The burden falls hardest on the communities least able to absorb it. Every utility will commission a lessons-learned report. Every report will identify the same gaps. And every recommendation will run into the same three constraints that created the crisis in the first place: contracts that cannot flex, markets that cannot coordinate, and a capacity gap that neither contracts nor markets, as currently designed, can close. These factors come together with a multitude of other political factors to create an energy trap closing in on utilities throughout Washington State. The first half of this paper describes the history and context, the second half is dedicated to how the region can work out from the trap.

1.2 The Coordination Scenario: January 2032

Now return to January 10, 2032. Imagine the same weather, the same cold, and the same five days below twenty degrees fahrenheit. Demand is spiking and generation is falling. BPA has called a system alert. Wholesale prices have spiked. The grid is starting to strain, but in this reality it doesn’t break.

In 2026, a coalition of Pacific Northwest utilities, state energy agencies, and tribal representatives established a coordinated resource adequacy framework that went beyond the Western Resource Adequacy Program’s compliance function. The coalition identified what this paper documents in Section 5: that utility integrated resource plans across the region contained assumptions about market access and resource costs that were mutually incompatible. Multiple utilities were counting on the same market purchases during the same stress events. The coalition created shared planning scenarios and, for the first time, checked whether the region’s individual plans added up. When the plans did not add up, stakeholders across the system pushed forward multiple baskets of solutions.

By 2028, Washington and Oregon had directed utilities to participate in coordinated transmission planning. BPA’s reconductoring program, accelerated by state legislative action, doubled capacity on three critical corridors using advanced composite core conductors on existing towers and rights-of-way. Cost: roughly half that of new line construction. Timeline: 18 to 36 months per corridor, not the 10 to 15 years a new transmission line requires. Dynamic line rating sensors, deployed across more than a thousand miles of regional transmission, monitored real-time conditions and identified 800 MW of available transfer capacity that the old static ratings would have left on the table.

State procurement authority, modeled on Illinois’s Clean and Reliable Grid Affordability Act and adapted for the Pacific Northwest’s institutional landscape, aggregated demand across six utilities. That aggregation gave developers the scale certainty needed to commit capital. The long-duration systems, iron-air batteries capable of discharging for 100 hours or more, were the technology that changed the calculus. For the first time, the region had storage that could ride through a multi-day winter event without solely depending on the Columbia’s seasonal flows.

But the grid of 2032 is not just a bigger version of the grid of 2025. It has changed in kind. By 2032, the Pacific Northwest had built what the old system never had: a distributed energy layer operating alongside the bulk grid, not as a collection of pilot projects but as coordinated infrastructure. Companies specializing in residential battery deployment had installed tens of thousands of home storage systems across the region, manufacturing, installing, owning, and operating them as a fleet. To each homeowner, the battery was affordable backup power and lower bills. To the grid, it was a virtual power plant, hundreds of megawatts of distributed capacity that could be dispatched in minutes. The Pacific Northwest adapted it for its own regulatory landscape: public power districts, investor-owned utilities, and tribal utilities each found structures that worked within their governance frameworks.

Flexibility markets, modeled on platforms already operating at gigawatt scale in the United Kingdom, connected distributed resources to the grid operators who needed them. Water heaters, heat pumps, EV chargers, commercial HVAC systems, and building batteries all enrolled in aggregation programs that shifted load automatically when the grid called for it. The technology was not exotic. Smart thermostats and connected appliances had existed for years. What was new was the market infrastructure: standardized enrollment, transparent pricing, and automated dispatch that turned millions of individual devices into a coordinated resource. Every electrified home, every electric vehicle parked in a garage, every commercial building with a smart energy management system became both consumer and contributor.

Community microgrids, backed by the same long-duration storage reaching commercial scale for the bulk system, provided resilience where it mattered most. Rural communities in fire-prone areas of eastern Washington and southern Oregon could island from the grid during emergencies and sustain essential services for days. Tribal communities whose energy infrastructure had been chronically underfunded gained distributed generation and storage that reduced their dependence on a transmission system built to serve someone else’s priorities. Low-income neighborhoods that had borne the worst outages during past cold events gained backup capacity and bill management tools deployed under CETA’s equity provisions. The communities most exposed to grid fragility were the first to benefit from the new system, not the last.

During the January 2032 cold event, this distributed layer reduced peak demand by 400 MW across the region, not through emergency appeals for conservation but through automated, compensated, planned response. Cross-market scheduling protocols, negotiated through the Regional Organization for Western Energy governance framework, enabled resource sharing across the EDAM/Markets+ seam. BPA’s hydro operations balanced generation with salmon protections under emergency protocols developed with CRITFC in advance, not under duress. The protocols existed because tribal representatives had been in the room when the planning framework was built.

Rates increased throughout Washington State. However, the price increased predictably, with advance notice, and the households with the least capacity to absorb price spikes had distributed resources that helped them manage the impact. The burden was shared. It was not equal, but it was visible, and it was planned for.

No blackouts. No emergency gas procurement. No impossible choices between the lights and the river.

The Coordination Scenario is not the absence of problems. It is the presence of institutions and infrastructure capable of managing problems that no single utility can solve alone: a bulk system strengthened by coordinated transmission and long-duration storage, and a distributed layer that turns every building and vehicle into a participant in the grid’s resilience. The Pacific Northwest built one of the world’s great energy systems on one river’s power. This scenario imagines a system built on the same region’s wind, sun, storage, and the intelligence of a grid that learns from every node.

1.3 The Present Moment

The decisions that determine which of these futures the region inhabits are being made right now. Many of these decisions have already been made or are seeing decisions windows rapidly close.

In December 2025, BPA countersigned Provider of Choice contracts locking in utility power allocations through 2044. In December 2024, BPA chose Markets+ over EDAM, splitting the Western day-ahead market into two competing platforms. E3’s April 2026 final resource adequacy study measures the Greater Northwest shortfall two ways. Against existing and committed resources alone, the region is 8,689 MW short by 2030, roughly the generating capacity of the state of Oregon. Against existing, committed, and currently in-development resources, the gap narrows to 5,600 MW across the Greater Northwest and 2,600 MW within the Pacific Northwest subregion specifically. An independent review commissioned by GridLab, treating coal-to-gas conversions as retained capacity rather than retirements, estimates the 2030 need at 1.0 to 4.9 GW depending on load growth. The range itself is the point. The shortfall is not a single number. It is a function of what the region chooses to build, retain, and coordinate over the next four years.

Every utility in the region is deep in a planning cycle that will lock in resource decisions for a decade or more. The next round of utility rate cases will set prices through 2030+. Transmission investment decisions being made this year will determine what can be built, and where, for the next fifteen plus years. However, many of these planning processes are running on assumptions that the rest of this paper will show are collectively unrealistic.

The window for coordination is not closing. For some decisions, it has already closed. For others, it remains open but narrowing with each rate case filed, each contract signed, each planning cycle completed in isolation. This paper is an attempt to map the full landscape of these interlocking constraints, to surface the contradictions that individual utility planning cannot see, and to identify the specific institutional changes that could shift the region from the collision path to the coordination path.

1.4 The Three Crises and the Energy Trap

Three crises are converging simultaneously in the Pacific Northwest electricity system.

The Shrinking Federal Foundation: The BPA contracts that govern the region’s federal hydropower were just locked in for sixteen years, freezing each utility’s allocation while the underlying river system contends with warming water, declining snowpack, and tribal treaty obligations that require water for salmon passage. The federal foundation is not growing to meet demand. It is contracting.

The Fragmented Market: BPA’s choice of Markets+ over EDAM splits the Western day-ahead market into two competing platforms at the moment regional coordination matters most. The governance concerns that drove the choice are legitimate. The cost is real: less efficient dispatch, harder access to diverse resources during stress events, and no entity coordinating transmission planning across the seam.

The Widening Capacity Gap: Independent studies disagree on the magnitude but agree on the direction. The region needs more dependable winter capacity than current plans will deliver, and the resources utilities are building most aggressively contribute the least during the multi-day cold events that define reliability risk. Utilities are also no longer the only buyers — technology companies are acquiring shovel-ready projects directly, removing them from a pipeline already insufficient to close the gap.

These three constraints are not parallel problems. Each blocks the standard response to the others, and each tightens as the others tighten. Section 3 examines that interlock in detail.

1.5 The Stakes From Where You Sit

Different readers will arrive at this paper from different professional vantage points. The analysis that follows is designed to serve all of them, but the stakes land differently depending on where you sit.

If you build, install, or finance clean energy in the Pacific Northwest, the region desperately needs what you are building, and the institutional architecture has made it hard to build. The capacity shortfall is not an abstraction: somewhere between 1,000 and 8,700 megawatts of dependable winter capacity that does not exist yet. Closing it requires resources at every scale, from bulk transmission down to the battery in a customer’s garage. Distributed and utility-scale buildout are reinforcing, not competing — every megawatt residential storage, demand response, and rooftop solar can shave is one that does not have to fight through a congested interconnection queue at PPA prices already running 15 to 35 percent above what utilities budgeted. The paths forward would create the largest sustained clean energy deployment opportunity in the region’s history, and the distributed side can move faster than anything else in the pipeline.

If you care about climate, environmental justice, and the communities that bear the costs of an energy system they did not design, this paper documents how the energy trap’s consequences fall hardest on the people least able to absorb them. Emergency market purchases during the January 2024 cold event cost Snohomish PUD ratepayers $45 million in a single month, and those costs flow into rates. For households already spending more than 10 percent of income on electricity, every rate increase driven by planning failures is a transfer of institutional risk onto the people with the least capacity to manage it. The analysis of tribal treaty rights and CRITFC’s two-decade institutional leadership is the argument’s moral and analytical center: communities with the longest relationship to this landscape have been saying since 2003 that the system needs fundamental redesign, not optimization within a broken framework.

If you are a utility planner, state energy office staffer, or consultant who already knows most of the facts in this paper, the contribution is synthesis, not discovery. You know the BPA contract structure, the market fragmentation debate, the capacity numbers. What you may not have seen is what happens when all three constraints bind simultaneously, because no institution’s planning mandate spans all three. The region’s individual utility plans do not add up when read together: simultaneous import assumptions, overlapping resource claims, cost projections already overtaken by the market. These contradictions are visible only when someone reads across IRPs on the planning cycle’s own timeline. The gap between the region’s diagnostic capacity and its institutional capacity to act on what it knows is the problem this paper is trying to close.

If you sit on a utility board, serve on a city council with utility oversight, or vote on energy policy in the legislature, the decisions documented here are decisions you authorized, will be asked to authorize, or can influence. Your general manager signed Provider of Choice contracts in December 2025. Your next rate case will set prices through 2030 or beyond. Your board will take positions on WRAP participation, BPA product elections, and new procurement to close the gap between what BPA provides and what your community needs. The contracts run through 2044. The decisions that determine whether those contracts govern a resilient system or a fragile one are concentrated in the next three to five years.

Section 2: How We Got Here

The two futures described in Section 1 fundamentally diverge because of institutions, not technology or geography. Understanding why the PNW’s institutions constrain the responses available today requires tracing how they were built, what crises shaped them, and what assumptions they encoded as they developed.

2.1 The Machine Built for Abundance

The Bonneville Power Administration was created by the Bonneville Project Act of 1937 to market the electricity generated by Grand Coulee and Bonneville Dams. The founding logic was simple: the federal government had invested massively in Columbia River hydroelectric infrastructure, and someone needed to sell the power. BPA’s statutory mandate gave preference to public utilities and cooperatives, creating the region’s distinctive public power system. The Northwest Power Act of 1980 expanded that role, directing BPA to meet the firm power needs of its preference customers and to acquire new resources if needed.

For decades, the system delivered. The Federal Columbia River Power System, 31 hydroelectric projects generating approximately 9,089 average megawatts under normal water conditions, produced more electricity than the region consumed. BPA sold the surplus to aluminum smelters and other energy-intensive industries, and the cheap hydropower attracted still more of them. Savings from the cheap hydro power and hungry industries passed on to rate payers. Much of the region’s entire economic identity formed around the assumption of abundant, inexpensive electricity.

That assumption became institutional muscle memory as decades of slow and steady growth caused concerns, but no crippling crises. BPA’s contracting structure, its rate-setting methodology, and its relationships with more than 140 preference customers all optimized for a world where the federal system had power to spare. Senator Henry Jackson, writing in support of the Northwest Power Act in 1980, warned that the region’s “era of abundance has abruptly ended” and that it faced “substantial electric energy deficits for the foreseeable future.” He was right, briefly. Load growth stalled in the 1990s, energy efficiency programs exceeded their targets, and what had looked like approaching scarcity dissolved back into comfortable surplus. The institutional apparatus built for abundance survived its first test because the test turned out to be temporary.

But between Jackson’s warning and the return of surplus came the region’s most spectacular failure of energy planning, and the institutional scar tissue it left behind would shape decisions for decades.

2.2 The Scar: WPPSS and the Fear of Big Bets

In the 1970s, the Washington Public Power Supply System, a joint operating agency of 23 publicly owned utilities, set out to do what this paper’s Section 7 argues the region needs to do now: build large-scale generation capacity to meet projected demand growth. WPPSS committed to constructing five nuclear power plants simultaneously, using three different designs, managed by a board of farmers and small businessmen with no nuclear experience. The projected cost at the outset was $4.1 billion (~$16 billion today). By 1982, the estimate had reached $23.8 billion. The demand forecasts that justified the plants proved wildly wrong: conservation measures spurred by the oil crises of the 1970s, combined with economic recession across the Northwest, eliminated the projected need entirely. Two plants were canceled, two were mothballed, and only one, Columbia Generating Station, was completed. In July 1983, WPPSS defaulted on $2.25 billion in municipal bonds, the second largest municipal bond default in U.S. history and rewriting municipal bond bankrupting terms for the country. The agency acquired a nickname that stuck: “Whoops”.

The financial damage was enormous, but the institutional damage ran deeper. Oregon’s 2025 Energy Strategy still references WPPSS as a “cautionary tale where over-investment and cost overruns led to the largest municipal bond default in US history.” In several of this paper’s author’s view, the region’s public utilities drew a lesson from WPPSS that was correct in the specific and damaging in the general: big capital bets on generation are dangerous. That lesson reinforced dependence on the existing hydroelectric system and on bilateral contracting rather than new construction, breeding an institutional conservatism around large-scale energy investment that persists today. It is visible in the slow pace of transmission development, the reluctance to commit to large scale capital projects, and the preference for incremental procurement over transformative buildout. The region that needed to learn how to build better instead learned to be afraid of building at all.

WPPSS was renamed Energy Northwest in 1998. Columbia Generating Station continues to operate, licensed through 2043. But the psychological infrastructure of the failure, the deep institutional wariness of ambitious generation projects, never got a name change.

2.3 The Crisis That Taught the Wrong Lesson

In 2000 and 2001, the Pacific Northwest experienced what the Northwest Power and Conservation Council later described as a “perfect storm.” Drought reduced hydro output while the California deregulation disaster pulled power south, and market manipulation by Enron and others drove wholesale prices to unprecedented levels. BPA had overcommitted its system. The result was an emergency: curtailed industrial loads, power purchases at extreme cost, and roughly $4 billion in losses to BPA customers.

The crisis revealed what happens when reliability pressures collide with the Columbia River’s other obligations. The Columbia River Inter-Tribal Fish Commission documented that in 2001, just 6 percent of juvenile steelhead survived their in-river migration from Lower Granite Dam to Bonneville Dam. In normal years, the survival rate runs 40 to 70 percent. When the choice narrowed to keeping the lights on or protecting salmon, the salmon lost. Treaty-protected fishing rights held by the Yakama, Nez Perce, Umatilla, and Warm Springs tribes were overridden by an emergency that the system’s own planning failures had created. Those rights are the foundation of tribal economies and predate the federal hydroelectric system by centuries. CRITFC’s response was direct: the tribes developed their first Energy Vision in 2003 specifically to prevent the region from ever facing that choice again.

The NWPCC identified the root cause in blunt terms: the problem was “inaccurate energy forecasting by the region’s electric utilities and Bonneville.” However, the institutional response optimized for the wrong variable. Rather than building mechanisms for flexible regional coordination, the region’s utilities and BPA spent the next seven years negotiating a framework designed above all for contractual certainty. That framework became the Regional Dialogue, a process where the BPA decided how subsidized energy would be divided between utilities. The choice was understandable: the region had just suffered two traumatic planning failures in two decades, WPPSS from overbuilding and the 2001 crisis from overcommitting. The instinct to lock down certainty, to nail the contracts shut so tightly that neither failure could recur, was rational. These contracts also were the beginning of the energy trap.

2.4 From Regional Dialogue to Provider of Choice

The Regional Dialogue, negotiated between 2002 and 2008, was the most extensive contracting process in BPA’s history. More than 130 public utilities and their representatives spent six years designing the framework that would govern the federal power system’s customer relationships. The central innovation was the Contract High Water Mark: each utility received a fixed allocation of cheap Tier 1 power based on its historical load, with consumption above that mark priced at Tier 2 rates reflecting the marginal cost of acquiring additional resources. The logic was transparent. BPA’s hydroelectric system was a finite resource. Allocating it based on demonstrated need, then pricing growth at its true cost, created both fairness and efficiency incentives. Conservation was rewarded. Growth bore its actual price.

The contracts signed in 2008 covered fiscal years 2011 through 2028, seventeen years. They included a flexibility mechanism that matters more now than it did then: Contract High Water Marks were recalculated each rate period, every two years, allowing allocations to adjust as loads shifted. The mechanism was imperfect, but it meant that utilities whose circumstances changed dramatically were not locked into decade-old calculations.

The Provider of Choice process, launched by BPA in 2020 and concluded with contracts signed in December 2025, carried the Regional Dialogue framework forward for [another sixteen years, through fiscal year 2044][pc-poc-contracts-through-2044-16-years]. It made one change that transforms the system’s character: [Contract High Water Marks are now fixed for the full contract duration. They are calculated once, based on fiscal year 2026 loads, and do not adjust.][pc-chwm-fixed-fy2026-no-adjust] Load growth receives only a 25 percent add-back. Conservation earns a 50 percent credit. The base allocation is frozen. And the policy landscape surrounding these contracts had shifted in ways the Regional Dialogue’s designers never anticipated. [Washington passed the Clean Energy Transformation Act in 2019.][pc-washington-ceta-2019] Oregon followed with HB 2021. The framework built for managing hydropower allocations now had to function within a system being rebuilt around decarbonization mandates that did not exist when the first contracts were signed.

In a period of stable demand, the distinction between adjustable and frozen allocations would be minor. In a period where Snohomish PUD revised its load growth projection upward by 116 percent between its 2021 and 2025 integrated resource plans, where data centers are driving regional demand at four times the historical growth rate, where [BPA itself projects a transition from 960 average megawatts of surplus in 2026 to a 3,091 average megawatt deficit by 2035][pc-bpa-960amw-surplus-to-3091amw-deficit], and where E3’s April 2026 resource adequacy study independently locates a 2,600 MW winter dependable capacity gap in the Pacific Northwest subregion by 2030, freezing allocations for sixteen years creates a structural constraint that no individual utility can escape. A mandate designed for abundance becomes something different in an era of scarcity. BPA is now locked into selling every kilowatt-hour a constrained river system can produce, through contracts designed for conditions that no longer hold, at rates that punish the very growth its own customers are experiencing.

The [contracts were due December 5, 2025. BPA countersigned by month’s end.][pc-poc-contracts-due-dec5-countersigned] They are binding through 2044.

Section 3: The Energy Trap

The contracts described in Section 2 are the floor. What follows is a map of the building constructed on top of it, and an explanation of why the exits are harder to find than they appear.

3.1 First Principles: What a Functional Grid Looks Like

A common refrain is that each grid’s situation is its own unique snowflake based on region, customer base, generation, and many similar factors. A well-functioning electricity grid has three properties: it covers a large geographic area, so that a cold snap in Seattle can be offset by mild weather in Phoenix; it has flexible access to diverse resources, so that low water years or still winds do not leave the system dependent on a single fuel; and it coordinates dispatch across the full system, so that a megawatt generated cheaply in Montana reaches the load center in Portland rather than being curtailed while Portland fires up an expensive gas peaker.

These are the core reasons Regional Transmission Organizations (RTO) exist throughout most of the United States. RTOs exist to coordinate the grid between utilities across vast geographies. They are why the [Western Energy Imbalance Market (WEIM), which only partially optimizes dispatch across a subset of Western balancing authorities, has still generated approximately [$8 billion in cumulative benefits since 2014]]pc-weim-8b-cumulative-benefits expanding energy trading areas, improving the diversity of resources, and coordinating dispatch.

The Pacific Northwest violates all three principles simultaneously. The Western Interconnection contains 38 separate balancing authorities, more than any other region in the country, and those authorities are now splitting into two competing day-ahead markets. BPA’s power allocations are fixed for 16 years regardless of how conditions change and capacity gaps are emerging for almost every utility.

The Pacific Northwest possesses the continent’s most diverse energy portfolio: the largest hydroelectric system in the United States, world-class wind resources in the Columbia Basin and Montana, strong solar potential in eastern Oregon and Washington, geothermal resources, and an operating nuclear plant licensed through 2043. The region does not lack resources. It lacks the institutional architecture to use them. The three crises that follow explain why.

3.2 Crisis 1: The Shrinking Federal Foundation

BPA’s Provider of Choice contracts, signed in December 2025, fix each utility’s access to cheap federal hydropower through fiscal year 2044. The mechanism is the Contract High Water Mark: a ceiling on each utility’s Tier 1 allocation, calculated once based on fiscal year 2026 loads and frozen for the full contract term. Below the ceiling, power costs approximately $35 to $41 per megawatt-hour. Above it, Tier 2 rates roughly double that, reflecting the marginal cost of acquiring additional resources. BPA documented an 83 percent increase in Tier 2 rates between September 2023 and October 2025 alone.

The ceiling is hard. In the one-time 2026 CHWM calculation, load growth that occurred under Regional Dialogue receives only a 25 percent add-back. Self-funded conservation from 2012 through 2023 earns a 50 percent credit. But once Bonneville publishes final CHWMs, neither adjustment recurs. A utility that adds load in 2031 or invests in conservation in 2034 receives no CHWM increase for either. This is the structural break from the Regional Dialogue contracts that preceded it: those recalculated high water marks every rate period, roughly every two years, adjusting for changes in system capability and customer load. The [Provider of Choice framework calculates once and holds for sixteen years. Whatever a utility’s allocation looks like in 2026, that is its allocation in 2044][pc-chwm-fixed-16yr-vs-regional-dialogue].

For utilities whose loads are growing, the math is unforgiving. Snohomish PUD’s CHWM stands at 755 average megawatts. SnoPUD expects to exceed that allocation within the first year of the new contract. The above-CHWM gap grows to 42 average megawatts by 2030, 124 by 2035, and 200 by 2039 (the cap SnoPUD elected for long-term Tier 2 purchases). BPA supplies 76 to 85 percent of SnoPUD’s portfolio. When SnoPUD revised its load growth projection from 0.96 percent to 2.07 percent annually between its 2021 and 2025 integrated resource plans, a 116 percent increase driven primarily by electric vehicle adoption and building electrification, the implications for its BPA relationship changed substantively, not marginally.

Seattle City Light occupies a different position but faces constraints that have worsened dramatically since its last planning cycle. SCL’s estimated CHWM of roughly 600 to 650 average megawatts (based on FY 2010 loads) reflects a utility where BPA supplies approximately 40 percent of the portfolio rather than 80 percent. SCL’s substantial owned hydroelectric generation at Boundary and Skagit dams provides a buffer that SnoPUD does not have. On paper, SCL looked more insulated from the CHWM squeeze.

Then the capacity requests started arriving. In July 2025, SCL’s General Manager Dawn Lindell told the utility’s Review Panel that the situation had changed in kind: “We need to double our nameplate capacity in the next 9 years.” The 2024 IRP showed SCL needed to add 1,825 MW of new nameplate generation to meet transportation electrification, building electrification, and city growth, plus 118 MW of additional conservation. But the IRP was barely published before the numbers moved underneath it. Between April and December 2024, SCL received more than 1,100 MW of new capacity requests, including several data centers, additional university load, and new industrial and commercial customers. Dawn Lindell’s assessment was blunt: while some of it will not materialize, 800 MW of it “actually looks pretty firm,” meaning the utility had severely underestimated its needs. SCL’s plan now calls for wind, solar, geothermal if available, and small modular reactors as baseload, with batteries for single-day peaks. Every megawatt added will cost more than the utility’s current power. [SCL’s 2022 IRP assumed solar PPA costs of $40 to $60 per megawatt-hour, assumptions the market has moved well beyond][pc-scl-2022irp-solar-ppa-40-60]. The 2026 IRP will have to reckon not just with a changed resource landscape but with a demand picture that shifted faster than the planning cycle could track.

And the system generating BPA’s power is not growing to meet the demand pressing against these allocations. Snowpack is declining, shifting when water arrives at the dams and how much energy they can generate. Tribal treaty obligations, honored through law, policy, and court orders, require increased spill for salmon passage, reducing the water available for turbines. Some hydroelectric facilities face relicensing processes that can take a decade, and their owners may choose to decommission rather than relicense as dams reach the end of their projected life and require costly updates and retrofits. The Columbia River Treaty with Canada, renegotiated in 2024, adds another layer of uncertainty about cross-border flows.

BPA itself projects a transition from 960 average megawatts of surplus in 2026 to a 3,091 average megawatt deficit by 2035. E3’s April 2026 study documents a 2,600 MW winter dependable capacity gap in the Pacific Northwest subregion by 2030, arrived at through separate methods and measuring a different quantity than BPA’s energy projection. Two analyses, two frames, one direction. The federal foundation is not just failing to grow. It is shrinking under the feet of the utilities that depend on it.

This is the floor of the trap. Utilities cannot simply buy more from BPA. The ceiling is fixed for Tier 1 subsidized rates. Above it, costs roughly double. And the system beneath that ceiling is losing capacity to the physics of a warming climate and the legal obligations of treaties that predate the dams themselves.

3.3 Crisis 2: The Fragmented Market

In December 2024, BPA chose to join SPP’s Markets+ rather than CAISO’s Extended Day-Ahead Market. To understand why that sentence carries such weight, you need to know what these two markets are. Starting in 2014, CAISO (the California Independent System Operator) offered the WEIM as a voluntary real-time trading platform. It worked well and grew to cover most of the Western Interconnection. The natural next step was extending that coordination to the day-ahead market, where utilities commit generation and lock in schedules for the following day. Two competing platforms emerged. CAISO proposed the Extended Day-Ahead Market (EDAM), building on the WEIM’s existing footprint. The Southwest Power Pool (SPP), which runs the grid across the central United States, proposed Markets+, designed with an independent governance structure outside any state’s grid operator. The economic case favored EDAM: a larger market captures more trading benefits. The governance case favored Markets+: BPA and many Western utilities viewed CAISO as California-controlled and feared subordinating their ratepayers to decisions made in Folsom. BPA’s December 2024 decision to join Markets+ split the West’s largest transmission owner away from the platform most Western load was expected to join.

The cost of that choice is quantified by multiple independent analyses, and the numbers are large. E3’s own economic evaluation found that EDAM would deliver $69 to $221 million more per year in benefits to BPA customers than Markets+. The Brattle Group’s analysis estimated that EDAM with BPA participation would generate $700 million per year in regional benefits, compared to $300 million without, and concluded that Markets+ may produce a net loss compared to the current status quo. Grid Strategies found that introducing a market seam where none currently exists reduces benefits by approximately two-thirds. These dollar figures capture part of what the market split costs, however they do not capture the most damaging consequence for the region’s capacity challenge.

This paper is not relitigating BPA’s market choice. The governance concerns that drove the decision are legitimate. Markets+ supporters have documented operational issues with CAISO, including load biasing that favors California’s balancing authority and Resource Sufficiency Evaluation failures that have left participating utilities exposed. These are substantive criticisms, not merely political ones. And California’s AB 825, signed in September 2025, creates the Regional Organization for Western Energy (ROWE), a path toward the independently governed market that BPA and its supporters have long called for. The governance problem has a proposed solution on the table. The question is what the fragmentation does in the years it takes to get there.

Three consequences matter for the capacity crisis.

First, the region loses unified transmission planning. Two market operators will generate competing investment signals. FERC staff, in their November 2025 whitepaper on Western seams coordination, identified the core structural difference: unlike Eastern RTOs, EDAM and Markets+ participants will not transfer functional control of their transmission systems to the market operator. Balancing authority areas remain distinct. Transmission availability is still primarily modeled using contract-path methods rather than the flow-based modeling used in the East. The result is a system where nobody plans transmission for the whole region, because no entity has the authority or the data to do so.

Second, utilities contracting for generation on one side of the seam face new friction wheeling power to load on the other. A Washington utility that signs a wind PPA with a Montana project may find that delivering that power across the EDAM/Markets+ boundary involves scheduling complications, congestion costs, and reliability protocols that did not exist when the contract was signed. FERC staff warned that seams coordination in the West will involve more parties and more complexity than the Eastern seams agreements that took decades to develop.

Third, and most consequential for the argument of this paper: no central actor exists to translate the region’s approaching capacity shortfall into coordinated, investable development signals. When a developer considers building a 500 MW wind farm in the Columbia Basin, they need to know which market platform the power will serve, whether delivery transmission will exist, and whether the project can attract a long-term contract. With two competing markets, two sets of scheduling rules, and no entity optimizing for the regional picture, the investment signals are blurred. Developers face uncertainty about which platform to build for. Utilities face uncertainty about whether resources contracted on one side of the seam can be delivered to load on the other. The market split does not just cost money. It removes the institutional machinery the region would need to build its way out of the capacity gap.

3.4 Crisis 3: The Capacity Gap

E3’s Phase 1 Resource Adequacy Study, sponsored by 25 utilities, projects an 8,689 MW capacity shortfall across the Greater Northwest by 2030. That headline number is contested, and the contest matters.

GridLab and Sylvan Energy Analytics reviewed E3’s methodology and identified specific assumptions that may overstate the gap. E3 holds firm imports constant at 3,750 MW across the study period, but actual imports into the Greater Northwest exceeded that figure in 102 hours during the January 2024 cold event, reaching above 5,000 MW in the most constrained hours. E3 models Canadian Treaty entitlements as net exports in all hours, without accounting for Canadian storage that could support imports during extreme events. And E3’s ELCC (effective load carrying capability — the measure of how much dependable capacity a resource actually contributes) calculations use marginal values for individual resource types, which may not capture portfolio effects where the combined contribution of diverse resources exceeds the sum of their individual parts. Renewable Northwest has gone further, characterizing E3’s methodology as “fundamentally outdated and flawed” and arguing that technology costs have declined faster than the study model.

These critiques deserve engagement. GridLab’s own modeling, using more favorable assumptions about imports and large load flexibility, produces a range of roughly 0 to 4.9 GW of additional resource needed, depending on load scenario. That range is wide. Even at its lower bound, the region faces meaningful capacity needs during multi-day winter events. At the upper bound, the need approaches E3’s headline figure. The directional finding is not in dispute: the region needs more capacity than current plans will deliver, and the gap is widening.

One assumption in GridLab’s analysis deserves particular scrutiny because it is doing enormous analytical work. GridLab’s more optimistic scenarios depend on the premise that large loads, primarily data centers, can be placed on special tariffs allowing curtailment during winter stress events. Their own modeling shows the scale of what this requires: depending on scenario and clean resource buildout, large load curtailments range from 55 to 222 hours per year under January 2024 weather conditions. At the high end, that is more than nine consecutive days of curtailment. GridLab’s Finding #4 states directly that supporting reliable winter data center operations in the Pacific Northwest “will likely require resources with more energy availability during challenging winter events.”

The question is whether that curtailment assumption reflects anything close to commercial reality. Data centers exist to provide uninterrupted computing capacity. Their customers pay for availability measured in fractions of a percentage point. Amazon’s CEO has publicly identified power supply as the company’s single biggest constraint on growth. Amazon just spent $83 million acquiring its own generation in Oregon specifically to reduce its dependence on utility-delivered power. Google paid $4.75 billion for a developer’s capabilities. These are not companies that will accept being told their facilities must go dark for days or weeks during the winter months that coincidentally produce peak demand for AI training workloads. A resource adequacy framework that depends on data centers voluntarily curtailing 100 or more hours per year is a framework that has assumed away the problem rather than solved it.

What matters more than the precise number is what kind of gap it is. The Pacific Northwest’s reliability risk is defined not by a four-hour evening peak (the kind of event that batteries handle well) but by multi-day winter cold events where temperatures drop below 20 degrees for five or more consecutive days, wind generation collapses under blocking high-pressure systems, and cloud cover eliminates solar output. During these events, the resources utilities are building most aggressively contribute the least. E3 found that four-hour batteries provide only 3 to 6 percent marginal ELCC during critical winter periods. Eight-hour batteries improve to 6 to 9 percent. Onshore wind contributes 10 to 24 percent. Customer solar, 5 to 14 percent. Natural gas provides 92 to 93 percent.

The reason four-hour batteries contribute so little is counterintuitive until you grasp it, and then it becomes the most illuminating finding in the entire resource adequacy debate. The Pacific Northwest already possesses the continent’s largest fleet of energy-limited storage: the Columbia River hydroelectric system. The dams are, in effect, giant batteries, storing water behind concrete and releasing it through turbines when the grid needs power. Adding more short-duration storage on top of a system already rich in energy-limited resources yields diminishing returns. The first battery on a gas-heavy grid provides enormous value. The hundredth battery on a hydro-rich grid provides almost none, because the grid’s problem is not moving energy around within a day. It is sustaining output across a week-long event when every energy-limited resource is running down simultaneously.

PSE’s scenario analysis made this concrete: to match the capacity contribution of a single 1,000 MW gas plant (at 93 percent ELCC), the region would need roughly 9,400 MW of four-hour battery nameplate. [That is approximately the current installed battery capacity of the entire United States.][pc-pse-9400mw-bess-equivalence] And those batteries would need to be charged during the multi-day events when the wind is not blowing and the sun is not shining.

Execution barriers compound the problem. Nationally, only 13 percent of generation projects submitted to interconnection queues between 2000 and 2019 reached commercial operation. Seventy-seven percent were withdrawn. Average timelines stretch beyond five years. BPA’s own queue contains roughly 120 GW of proposed projects (49 GW solar, 21 GW wind, 51 GW storage), but historical completion rates run 10 to 15 percent. Wind power purchase agreements now cost $67 to $77 per megawatt-hour, rising 14 percent year-over-year, well above the $40 to $55 per megawatt-hour that most utility plans assumed. Battery storage costs have risen 56 to 69 percent above 2023 projections. The One Big Beautiful Bill Act imposed a July 4, 2026 safe harbor deadline for projects to qualify for IRA tax credits. Projects that miss the deadline face effective cost increases of $10 to $20 per megawatt-hour.

And utilities are no longer the only buyers competing for these scarce resources. In January 2026, Amazon outbid Puget Sound Energy in a bankruptcy auction for Pine Gate Renewables’ Sunstone project in Morrow County, Oregon: 1.2 gigawatts of solar generation and 1.2 gigawatts of battery storage, fully permitted and shovel-ready. Amazon paid $83 million. PSE’s final bid was $82 million. For a one million dollar difference, a utility that needed the project to meet Washington’s clean energy mandates lost it to a technology company whose CEO had publicly identified power constraints as the single biggest bottleneck to its data center expansion. PSE’s senior vice president of external affairs captured the new reality: “We are used to being kind of the only buyers for these things as utilities, and now there are other buyers who are a little bigger than we are.”

The Sunstone acquisition is not an isolated event. It is the shape of the new market. Amazon had previously sued PacifiCorp in Oregon for failing to deliver adequate electricity to its data centers, with one campus receiving no power at all. Google acquired the energy developer Intersect Power for $4.75 billion. Technology companies are not waiting for utilities to solve the capacity problem. They are buying the solutions directly, at prices utilities cannot match, removing shovel-ready projects from a pipeline that was already insufficient to close the regional gap. Every gigawatt a technology company acquires for its own load is a gigawatt that does not serve the regional grid.

Whether the shortfall is 4,000 or 9,000 MW, the structural problem is the same: the region needs more capacity than current plans will deliver, the resources it is building contribute the least during the events that matter most, the execution pipeline is congested, expensive, and running out of federal support, and the buyers with the deepest pockets are pulling resources out of the shared pool for their own use.

3.5 The Trap Mechanism: How the Crises Interlock

Each of the three crises described above is, individually, a problem with well-understood responses. Utilities facing BPA allocation limits can buy from the market. Utilities facing market limitations can build their own resources. Utilities facing construction barriers can wait for conditions to improve. What makes the current situation a trap, rather than a set of parallel challenges, is that each crisis blocks the standard response to the other two. The exits are not merely difficult. They lead back into the building.

Walk through it in sequence.

Your BPA allocation is fixed. Your Contract High Water Mark was calculated based on FY 2026 loads. If load grows faster than expected — and SnoPUD’s experience suggests it might — you hit the ceiling. Above-CHWM load pays roughly double. You cannot buy more Tier 1 subsidized energy.

So you turn to the market. But the day-ahead market is splitting in two. BPA joined Markets+; CAISO runs EDAM. If you are on one side of the seam and the cheapest available resource is on the other, you face scheduling friction, congestion costs, and reduced transfer capability. During the multi-day winter events when you most need market access, the same cold snap is hitting every utility in the region simultaneously. Everyone is short at the same time. The fragmented market delivers the least precisely when the need is greatest.

So you try to build your own resources. But the interconnection queue completion rate is 13 percent nationally. Wind PPAs cost $67 to $77 per megawatt-hour, not the $40 to $55 in your IRP. Battery costs are 56 to 69 percent above projections. The IRA safe harbor deadline is July 4, 2026. And you are now competing for equipment, labor, and interconnection capacity not just against other utilities but against technology companies whose capital expenditure budgets exceed the combined revenue of every utility in the region.

Each constraint tightens the others. Fixed BPA allocations push more utilities into the market, increasing competition for limited market resources. Market fragmentation prevents efficient resource sharing, widening the effective capacity gap. The wider capacity gap means more utilities are desperate to build, further congesting the interconnection queue and driving up PPA costs. The system is not just failing in three places. It is failing in a way where each failure makes the other two worse.

SnoPUD illustrates the trap in detail because its data is the richest and its exposure is the most clearly documented, but the logic applies across the region. SnoPUD’s optimization model selected maximum BPA Tier 2 purchases (200 average megawatt cap) in every scenario it tested. Not because Tier 2 is cheap (it is roughly double Tier 1). Not because it is optimal, but because every other option is worse. That is the energy trap in action: when the best available strategy is to pay double for the same federal hydropower you were getting at Tier 1 rates, the system has failed at the level of its design.

The trap is tighter for some utilities than others. Utilities heavily dependent on BPA (SnoPUD at 76 to 85 percent) face the most severe CHWM exposure. Utilities with substantial owned generation (SCL with Boundary and Skagit, Chelan and Grant with their own Columbia River projects) have more flexibility on the BPA dimension, though as SCL’s experience shows, that buffer is shrinking fast. No utility in the region is immune to a shortfall that approaches the generating capacity of the state of Oregon, and no utility can unilaterally solve a coordination problem that is regional in scale.

The natural response to the energy trap is to look to regions that are building better tools. The Pacific Northwest has no capacity market, no single grid operator, no centralized procurement mechanism. Surely a region that has all of those things would handle a demand surge and a constrained generation fleet more effectively. Before turning to how Pacific Northwest utilities are planning within these constraints, it is worth testing that assumption against the one region in the country best equipped to disprove it.

Section 4: The PJM Detour

The PJM Interconnection is the overachiever of American electricity. One regional transmission organization spanning 13 states and Washington, D.C., serving 67 million people. Centralized energy markets, capacity markets, ancillary services markets. Regional transmission planning coordinated across the entire footprint. PJM has been running these systems longer than any other RTO in the country. If any grid operator should be able to handle the collision between rising demand and a constrained generation fleet, it is PJM. As utility planners, policymakers, elected officials, and ratepayers have discovered in sequence over the last three years, PJM cannot.

4.1 The Capacity Market Breaks

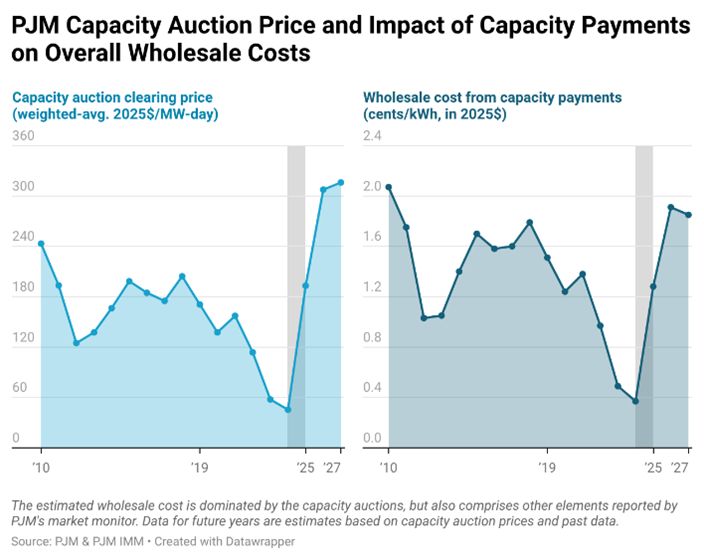

PJM’s capacity market was designed to solve the problem the Pacific Northwest now faces. Generators get paid years in advance to commit to being available when the grid needs them. Utilities cannot always own their own generation in wholesale market regions. Capacity markets are additional to energy and ancillary service markets and are used to send supplemental price signals to generators that new supply is needed to meet electricity demand during periods of grid stress. When capacity is tight, prices rise to attract new investment. When supply is abundant, prices fall to signal retirements. The mechanism is elegant in theory and works during periods of stable growth. In practice, it has broken down in a sequence that this paper’s readers should study carefully, because the same forces are at work in the Pacific Northwest without even the market signals to make them visible.

Each year, the capacity auction determines a price to clear that in turn will be paid by the region’s utilities and then ratepayers. For the 2024/2025 delivery year, PJM’s capacity auction cleared at roughly $29 per megawatt-day. For 2025/2026, it spiked to $269.92. For 2026/2027, prices hit a FERC-approved cap of $329.17. For 2027/2028, they hit the cap again at $333.44. Three consecutive record-breaking auctions, each clearing at or near the ceiling. PJM estimates that without Governor Shapiro’s negotiated price collar, the 2027/2028 auction would have cleared near $530 per megawatt-day. The collar saved ratepayers an estimated $10 billion in a single auction year. The market designed to prevent exactly this kind of price escalation instead produced it.

Even at the capped price, PJM could not buy enough capacity. The 2027/2028 auction fell 6,623 MW short of PJM’s reliability requirement: the gap between what the system procured and the 20 percent reserve margin that PJM calculates it needs to prevent more than one unexpected outage every ten years. Reserve margins dropped to 14.8 percent, the lowest PJM has ever recorded. This was the first time the entire RTO, including utilities that self-supply their own capacity outside the auction, fell below the reliability standard. PJM retains enough generation to keep the lights on under normal conditions. The margin for abnormal conditions, the margin that exists precisely because conditions are not always normal, has shrunk to the thinnest buffer in the organization’s history.

The capacity market’s theory holds that high prices attract investment to build new energy generation. A gas plant developer seeing $333 per megawatt-day should be racing to build. But a gas plant responding to the 2024 price signal will not come online until 2031 or 2032, a lag of seven to eight years that covers permitting, siting, interconnection studies, and construction. Battery storage can be built in roughly 18 months. But PJM’s interconnection queue was effectively closed to new entry from 2022 through spring 2026 while the operator cleared a 200 GW backlog. The 2027/2028 auction attracted only 774 MW of new generation. The price signal worked, however the system that goes into building new generation could not respond.

PJM’s governance helps explain the slow institutional response. The stakeholder process has over 1,000 voting members. Fourteen of them are state-appointed consumer advocates. The rest represent the regulated industry. As Clara Summers of the Citizens Utility Board described it in February 2026: it is the regulated industry setting the rules for itself. Twelve reform proposals addressing data center interconnection and capacity procurement went to an advisory vote in November 2025. None of these proposals reached consensus.

4.2 The Data Center Lesson

The force driving PJM’s crisis is the same one reshaping the Pacific Northwest: data centers. In PJM’s latest forecast, data centers account for nearly all of the 5,250 MW increase in peak load, roughly 97 percent. Virginia alone hosts some 643 data center facilities, more than any other state. The Dominion Energy zone expects 20,000 MW of additional data center load by 2037.

The political response has been vigorous and, so far, ineffective at slowing the physical demand. Virginia’s State Corporation Commission approved a new rate class for large customers in November 2025, requiring data centers to pay for at least 85 percent of their contracted distribution and transmission demand. In the 2026 legislative session, Virginia lawmakers introduced bills to shift infrastructure costs to data centers, condition interconnection on grid readiness, and study moratoriums. PJM’s own market monitor told the operator to stop connecting new data center loads until infrastructure catches up. PJM responded that it has no authority to refuse service.

The lesson from PJM is not that data center demand projections are accurate to the megawatt. They are likely overstated. The lesson is that even overstated projections produce real consequences, compounded by existing electrification and the upgrades needed to maintain an aging, climate-exposed grid. The demand that does materialize arrives faster than infrastructure can be built to serve it, concentrates in ways that overwhelm local systems, and comes backed by capital budgets that make regulatory friction a minor inconvenience rather than a binding constraint. Douglas County PUD imposed a moratorium on new data center contracts in 2019 after 40 percent load growth in three years. Grant County PUD’s queue contains 2,897 MW from 75 applicants, with wait times of seven to ten years for new service. The demand did not disappear. It queued into other areas in the grid.

4.3 What the Comparison Proves, and What It Does Not

The Pacific Northwest has none of what PJM has built. Thirty-eight separate balancing authorities instead of one. No capacity market. No centralized transmission planning. A day-ahead market that is splitting in two. This comparison is not an argument that the Pacific Northwest should adopt PJM’s model, and the differences between the regions are real. PJM’s resource mix is fossil-heavy where the Pacific Northwest is hydro-dominated. PJM peaks in summer; the Pacific Northwest peaks in winter. The region’s hydroelectric system provides built-in storage and flexibility that PJM’s fleet does not have. And the Pacific Northwest explicitly chose not to build a capacity market.

What the comparison does is close off two comforting assumptions. The first is that better market mechanisms would solve the problem. PJM has the most mature capacity market in the country. It still faces a 6,600 MW reliability shortfall, three consecutive capacity price caps, and a timeline mismatch between demand growth and supply response. The second is that regulation can contain the demand. At least 12 states are trying. The demand keeps coming, backed by [companies whose quarterly capital expenditures exceed the annual revenue of most utilities][pc-12-states-demand-regulation]. The tools everyone assumed would handle this transition, centralized markets, interconnection processes, legislative oversight, are proving less reliable than anyone thought, in the regions with the best versions of those tools. Attempts to intervene in PJM processes and the interconnection queue have drawn mixed results and a flurry of high-stakes, costly lawsuits.

Other states have begun drawing different conclusions. Illinois, facing the same PJM capacity price spikes and split between two RTOs (PJM and MISO), decided that federal market mechanisms were too slow. In January 2026, Governor Pritzker signed the Clean and Reliable Grid Affordability Act, empowering the Illinois Commerce Commission to directly procure clean energy and storage capacity at the state level. Section 7 will return to what the Pacific Northwest can learn from that choice.

The decisions that determine whether the energy trap tightens or loosens are being made right now, largely inside utility integrated resource plans. The next section examines what happens when individual utilities try to plan their way through a regional problem that their planning tools were not designed to see.

Section 5: How Utilities Are Planning

5.1 The Core Contradiction

An Integrated Resource Plan is a utility’s answer to a deceptively simple question: how will you keep the lights on for the next twenty years, and what will it cost? Every major utility in the Pacific Northwest filed or updated an IRP between 2022 and 2025. Snohomish PUD adopted its plan in December 2025. Seattle City Light is developing its 2026 IRP. Puget Sound Energy is building the state’s first Integrated System Plan, merging resource planning with clean energy compliance into a single document due January 2027. Avista filed its 2025 IRP. Portland General Electric and PacifiCorp filed plans in 2023. Each of these documents represents months or years of analytical work by teams of engineers and economists modeling thousands of scenarios.

Each plan may be internally rigorous. The problem only appears when you lay them side by side. Neighboring utilities serving the same region, subject to the same weather, drawing from the same BPA system and regional wholesale market, are making materially different assumptions about the same future. They cannot all be right. If every utility in the region assumes it can buy power from the market during a winter cold snap, and every utility is short at the same time, the market they are counting on does not exist. If one utility models wind costs at $54 per megawatt-hour and its neighbor across the county line uses market data showing $67 to $77, one of those plans is building a portfolio it cannot afford.

This is not a competence failure. It is a coordination failure. The IRP process is designed to optimize for a single utility’s customers. No mechanism exists to check whether the region’s individual plans, taken together, describe a future that is physically possible. PNUCC, the organization that produces the only regional utility-perspective forecast, states explicitly that its work is “NOT a resource adequacy assessment.” The Northwest Power and Conservation Council’s Ninth Power Plan attempts a regional synthesis, but it updates only every five years. Utility planning cycles run two to four years. The gap between them is where the contradictions hide.

5.2 The Assumption Contradictions

Six categories of planning assumptions diverge across the region’s utilities. Each divergence, examined alone, reflects a defensible judgment call under genuine uncertainty. Examined together, they reveal a set of plans that cannot all succeed simultaneously.

How fast is load growing?

Snohomish PUD revised its base case load growth from 0.96 percent to 2.07 percent annually between its 2021 and 2025 IRPs, a 116 percent increase driven primarily by electric vehicle adoption and building electrification. Avista moved in the same direction but more modestly, increasing its energy forecast growth from 0.24 percent to 0.85 percent annually, citing higher EV projections. Seattle City Light’s 2026 IRP load forecast is, in its own description, “similar to the last load forecast,” with slight shifts between residential and commercial mix and new “spot loads” incorporated in later years. SCL remains somewhat insulated from data center demand by its 131-square-mile urban service territory. PSE, serving the region’s largest investor-owned utility territory, is modeling three deficit categories simultaneously in its ISP framework: effective peak capacity, renewable and non-emitting resource requirements, and total energy.

At what scale, regionally?

At the regional level, the numbers are harder to reconcile. PNUCC’s 2025 forecast projects loads growing by approximately 7,800 average megawatts over the next decade, reaching 31,600 aMW by 2034, an increase of more than 30 percent. The NWPCC’s initial Ninth Power Plan scenarios range from 26,000 to 31,000 aMW by 2030, a 5,000 aMW spread driven largely by data center uncertainty. The PNUCC ten-year energy growth rate has climbed from 0.9 percent in its 2022 forecast to 3.2 percent in 2025. That is not a modest revision. That is a different planning universe.

If SnoPUD’s 2.07 percent growth trajectory materializes across the region, the capacity gap documented in Section 3 is far larger than current estimates suggest. If SCL’s flatter trajectory holds, the gap is more manageable. Both utilities draw from the same BPA system and the same regional market. They are planning for different futures and it is important to understand differences in the cost of projects in these futures.

At what cost?

SnoPUD’s 2025 IRP assumes wind PPA costs of $54 to $58 per megawatt-hour. Current market prices for wind PPAs run $67 to $77 per megawatt-hour, a gap of $13 to $19. SCL’s 2022 IRP assumed solar PPA costs of $40 to $60 per megawatt-hour, assumptions the market has moved well beyond. Battery storage costs industry-wide have risen 56 to 69 percent above 2023 projections.

Every utility’s optimization model selects resources based on cost inputs. If those inputs are 15 to 35 percent below actual market prices, the model produces a portfolio that looks balanced on paper but describes resources that may not be available at the projected price. The plans are optimizing for a market that no longer exists.

Will the market be there?

The assumption that the market will be there when you need it is the most dangerous assumption in Pacific Northwest resource planning. E3’s Phase 1 study holds firm imports into the Greater Northwest constant at 3,750 MW across the study period. GridLab critiques that figure as potentially understating market access, noting actual imports exceeded that threshold during the January 2024 cold event. But the deeper problem is structural. Multiple utilities assume the ability to purchase short-term energy from the market to cover gaps during stress events. If every utility in the region is short during the same multi-day winter event, the collective assumption of market availability is a plan built on power that does not exist. WECC’s 2024 assessment found demand growth across the Western Interconnection is “more than double” what utilities projected in 2022 resource plans, growing at four times the historical rate. Pacific Northwest utilities face competition for the same limited pool of market energy from utilities across the entire Western grid, at the same time technology companies are acquiring resources directly.

With how much margin?

Each of the utilities has a different reserve margin. Avista plans for a 24 percent winter reserve margin. PSE uses roughly 15 to 17 percent. PacifiCorp runs at 13 to 15 percent. The NWPCC has historically used a 5 percent loss-of-load probability standard considered less stringent than other regions. These are not different ways of expressing the same level of caution. A 24 percent winter PRM produces very different resource acquisition signals than a 13 percent PRM. If the region faces a common shortfall, the utility with the lowest reserve margin becomes the weakest link. Reliability failures do not respect utility service territory boundaries.

Which BPA product?

In late 2025, every BPA preference customer faced the same deadline: choose your power product for the next sixteen years. SnoPUD elected Load Following under the Provider of Choice contract after a comprehensive analysis comparing product options across multiple timeframes. The financial difference between product elections runs to hundreds of millions of dollars over the contract term, depending on assumptions about hydro conditions, market prices, and WRAP compliance costs. SCL’s BPA product choice is part of its 2026 IRP process. Each utility conducted this analysis independently, with different models, different assumptions about future conditions, under time pressure imposed by BPA’s contracting deadline, and without any mechanism for regional coordination. These may be the most consequential resource decisions Pacific Northwest utilities have made in a generation. Each utility made them alone.

5.3 What Models Cannot See

Even when individual IRPs are analytically sophisticated, three structural blind spots prevent them from seeing the energy trap.

The first is simultaneity. An IRP optimization model evaluates a single utility’s portfolio against a set of market and weather scenarios. It does not model what happens when every neighboring utility executes the same strategy at the same time. If SnoPUD, SCL, PSE, Tacoma Power, and Clark PUD all plan to acquire wind PPAs from Columbia Basin projects, they are competing for the same limited interconnection points, the same transmission capacity, and potentially the same developers. The models cannot see this competition because they model only one utility at a time. The result is a set of plans that each look feasible in isolation and become collectively impossible when they all hit the market simultaneously.

The second is interconnection reality. Most IRP models assume resources can be acquired at modeled costs and deployed on modeled timelines. The 13 percent historical completion rate for interconnection queue projects, and the five-plus-year average timeline from request to operation, are external constraints that models incorporate imperfectly if at all. SnoPUD’s IRP contains no explicit discussion of interconnection queue backlogs. SCL’s 2022 IRP assumed resource costs now significantly outdated. BPA reformed its queue process in June 2024, moving to a “first-ready, first-served” model, but 376 projects remain in the pipeline with [timelines stretching 900 to 2,330 days][pc-bpa-376-projects-in-pipeline]. A plan that assumes a wind farm will be online by 2029 may be describing a project that will not clear the queue until 2031.

The third is capital competition from outside the utility sector. IRP models assume utilities are the primary buyers of generation resources. They are not. The Sunstone outbid documented in §3.4 — Amazon taking a 1.2-gigawatt shovel-ready project from PSE for a one-million-dollar premium — is the canonical case, and it is not isolated. No IRP optimization model incorporates the possibility that the resources in its optimal portfolio will be acquired by a buyer with a capital budget larger than the utility’s total revenue.

The problem is not that IRP teams lack sophistication. PSE’s transition to an Integrated System Plan, Avista’s 24 percent winter planning reserve margin, SnoPUD’s multi-scenario optimization all reflect serious analytical work. The problem is that the IRP process is structurally designed to answer a single-utility question in a region facing a multi-utility crisis. It is the wrong tool for this challenge, deployed because no better regional mechanism exists.

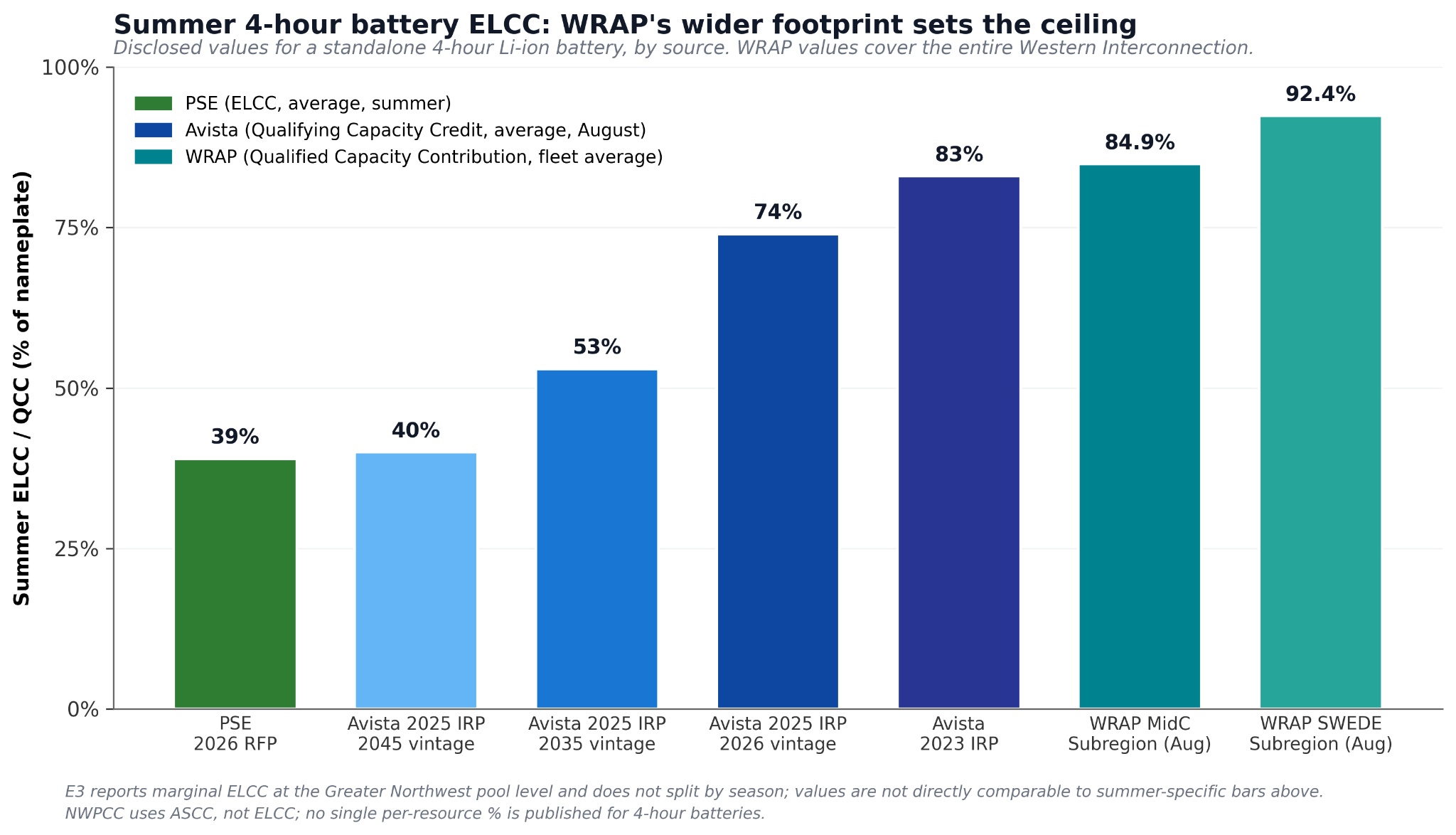

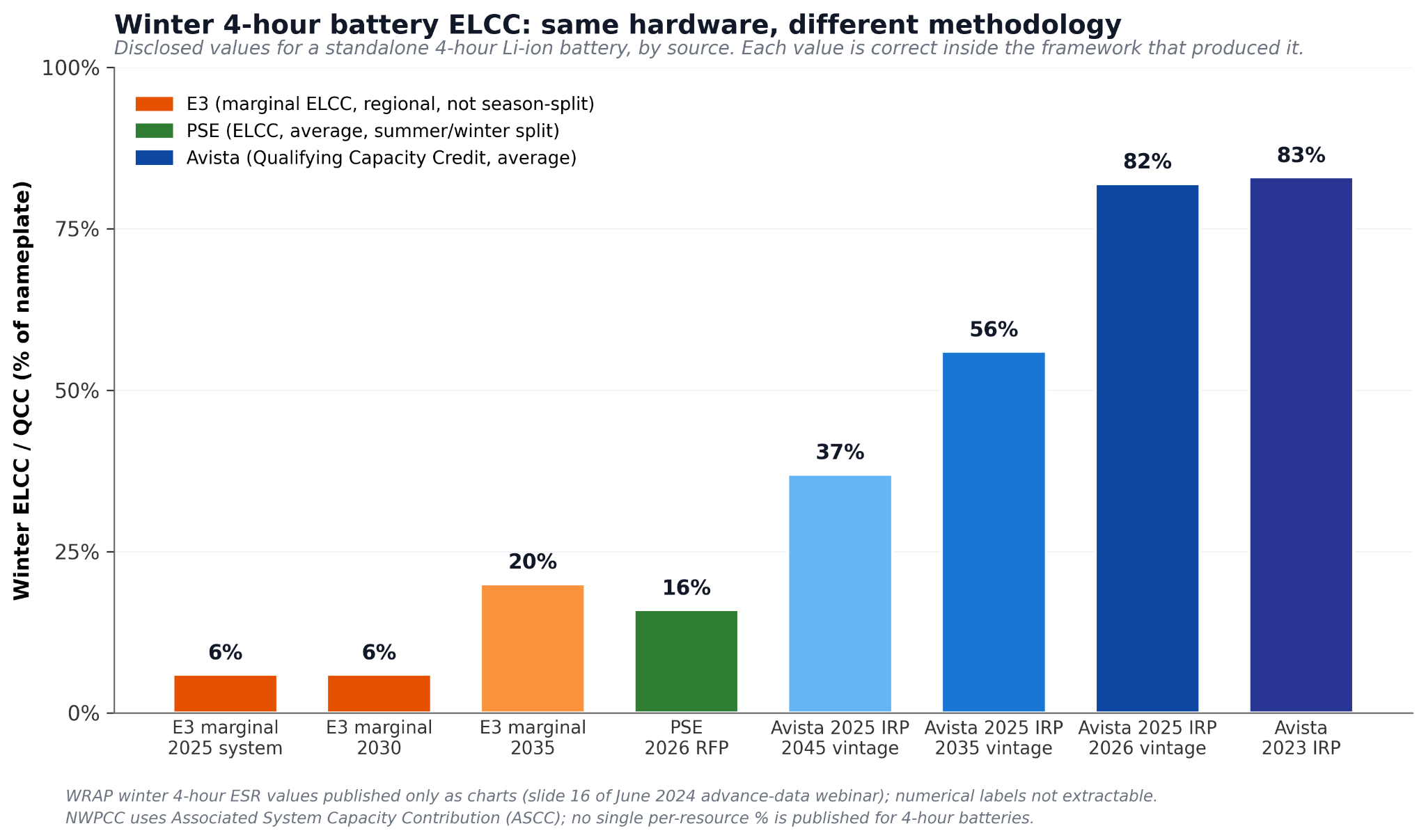

5.4 What Counts as a Megawatt

Avista’s 2025 IRP credits a 4-hour lithium-ion battery with an 82 percent winter capacity contribution. PSE’s 2026 utility-scale RFP credits the same battery class with 16 percent. Both numbers come from public regulatory filings made within months of each other, both describe a battery that would serve Washington customers, and both purport to answer the same question: how much of the battery’s nameplate capacity counts toward keeping the lights on at peak demand.